Smart Money Management 101: 5 Steps to Take Right After Payday

Breaking the Paycheck-to-Paycheck Cycle

Understanding the Struggle

Living paycheck to paycheck is a common challenge for many, regardless of income level. Rising costs of rent, groceries, and transportation, coupled with unexpected expenses like medical bills or car repairs, can drain a paycheck quickly. Without room to save or plan, financial stress becomes the norm, making payday more anxiety-inducing than exciting.

The Power of a Plan

The days right after payday are crucial for taking control of your finances. Without a clear plan, it’s easy to spend impulsively and leave little for future needs.

A smart money strategy ensures you allocate funds intentionally, protecting your goals and reducing financial stress. It’s about creating financial stability and empowerment—not about restriction.

Five Steps to Transformation

Managing money well doesn’t require perfection—it requires consistency and simple, intentional steps:

Track your income and build a realistic budget.

Pay yourself first by starting an emergency fund.

Tackle high-interest debt strategically.

Contribute to retirement accounts early and regularly.

Allocate money toward short- and long-term goals.

These foundational steps will help shift your financial mindset and create long-term habits for success.

Step 1: Track Your Income and Create a Budget

Understanding Your Take-Home Pay

Start by identifying your net income—the amount you receive after deductions for taxes, insurance, and retirement contributions. If your income varies, calculate an average from the past few months to get a reliable number. Knowing exactly how much money is coming in allows you to make informed decisions and avoid overspending.

Creating a Realistic Budget

List fixed expenses (rent, utilities, insurance) and variable expenses (groceries, transportation, entertainment). Don’t forget annual or irregular expenses like memberships or car repairs. Allocate a portion of your income to each category, leaving room for discretionary spending. A good rule of thumb is the 50/30/20 rule: 50% needs, 30% wants, 20% savings or debt repayment.

Tools to Simplify Budgeting

Apps like Mint, YNAB (You Need a Budget), and PocketGuard can help automate and visualize your spending. They link to your bank accounts and categorize expenses, making it easy to track patterns and stay on top of your budget goals. You can also use Google Sheets or Excel for a custom approach. Budgeting is the first key to achieving financial clarity.

Step 2: Pay Yourself First – Build Your Emergency Fund

Why Emergency Funds Matter

Life happens—unexpected bills, car trouble, or job loss can throw your finances off track. An emergency fund acts as a financial buffer, helping you stay out of debt when surprise expenses arise. It’s one of the most critical components of a strong financial foundation.

Setting Realistic Savings Goals

Start with $500 to $1,000 for minor emergencies. Eventually, aim for 3–6 months of essential living expenses. Your goal depends on your job stability, household size, and income consistency. Begin by saving $50 or $100 per paycheck until you reach your target.

Automate Your Savings

Set up automatic transfers from your checking to a separate savings account right after payday. Choose an account that’s out of sight and not tied to your debit card. Label it “Emergency Fund” to reinforce its purpose. Automation helps remove temptation and keeps your savings on track.

Where to Keep Your Emergency Fund

Choosing the right place to store your emergency fund money is just as important as building it. The goal is to keep your money safe, accessible, and growing, so you can handle unexpected expenses without stress or delays.

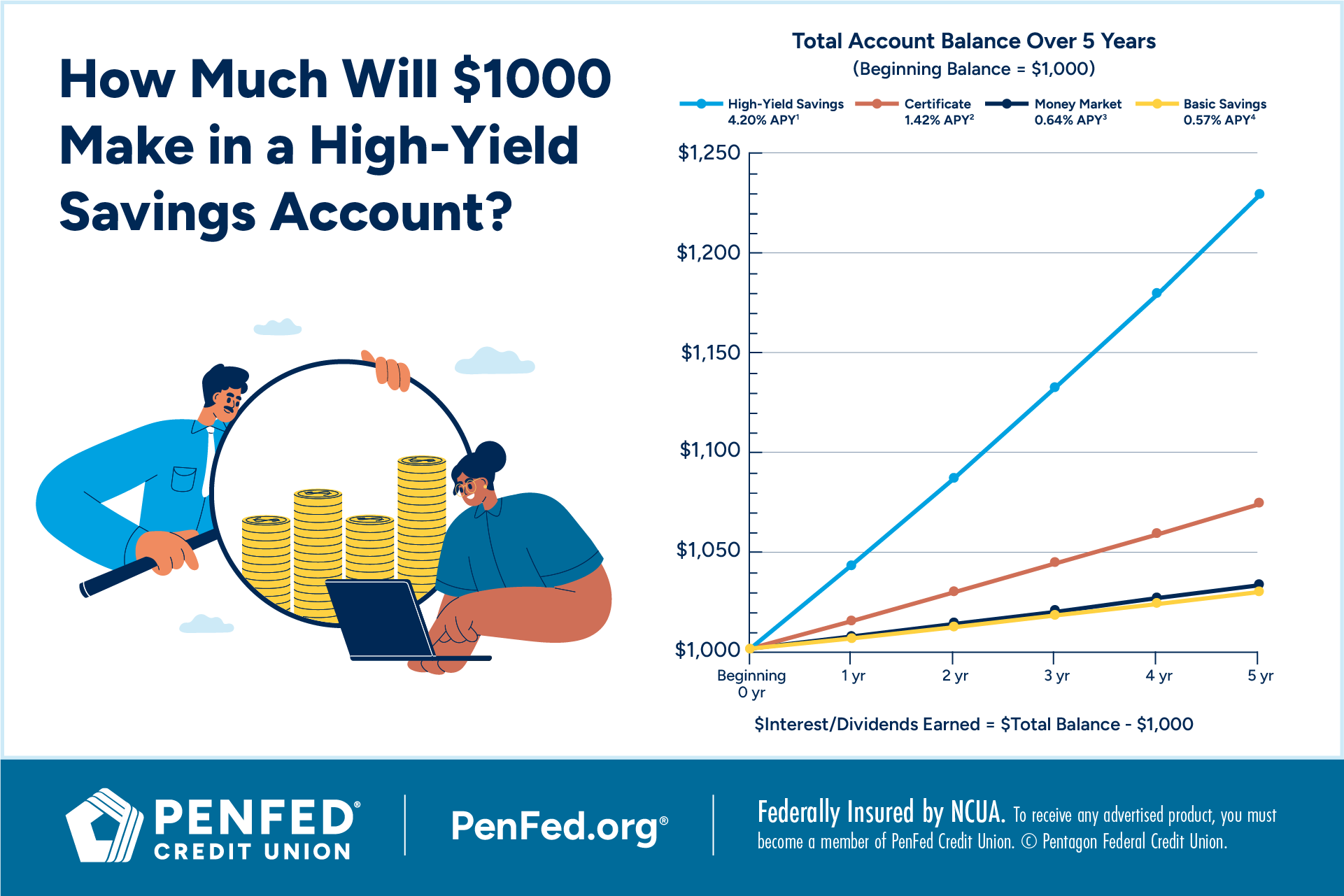

High-Yield Savings Accounts: The Best of Both Worlds

A high-yield savings account (HYSA) is one of the smartest places to keep your emergency fund money. Unlike traditional savings accounts that offer minimal interest, HYSAs provide significantly higher returns, allowing your money to grow while remaining liquid.

This means your emergency fund isn’t just sitting idle—it’s actively earning money while staying available when you need it most.

Why Online Banks Often Offer Better Rates

Online banks typically have lower overhead costs than traditional brick-and-mortar institutions. Because of this, they can pass those savings on to customers in the form of higher interest rates on your money.

Benefits of online savings accounts include:

Higher APYs (Annual Percentage Yields)

Lower or no monthly fees

Easy access through apps and online platforms

Fast transfers between accounts

This makes them an ideal choice for storing emergency fund money efficiently.

Safety First: FDIC Insurance Matters

No matter where you keep your emergency fund money, security should be a top priority. Always ensure your account is FDIC-insured (Federal Deposit Insurance Corporation). This protects your money up to $250,000 per depositor, per bank, in case the institution fails.

This level of protection means your money remains safe even in worst-case scenarios—exactly what an emergency fund is designed for.

Accessibility Is Key

While it’s tempting to chase higher returns, avoid locking your emergency fund money into investments or accounts that restrict access. In an emergency, you need your money quickly and without penalties.

Look for accounts that offer:

Instant or same-day transfers

No withdrawal penalties

Easy mobile access

Your emergency fund should be ready when you need it—not tied up or delayed.

The Bottom Line

The best place to keep your emergency fund money is where it can grow safely, remain accessible, and stay protected. High-yield savings accounts—especially from reputable online banks—offer the ideal balance between security, liquidity, and returns.

By choosing the right account, you ensure your money is not only protected but also working quietly in the background, helping you build a stronger financial safety net.

Step 3: Tackle High-Interest Debt

The Danger of High-Interest Debt

High-interest debt is one of the biggest obstacles to building long-term wealth. Credit cards, payday loans, and certain personal loans often carry interest rates of 20–30% or more, which means your money is working against you instead of for you.

Even small balances can quickly spiral out of control when you’re only making minimum payments. A large portion of your payment goes toward interest rather than reducing the principal, keeping you stuck in a cycle that’s difficult to escape.

Here’s why high-interest debt is so dangerous:

It drains your money through ongoing interest charges

It limits your ability to save and invest

It increases financial stress and reduces flexibility

The longer you carry this type of debt, the more money you lose—making it critical to prioritize paying it off as quickly as possible.

Avalanche vs. Snowball Method

When it comes to eliminating debt, two proven strategies can help you take control of your money:

Avalanche Method (Best for Saving Money)

Focus on paying off debts with the highest interest rates first, while making minimum payments on the rest. This approach minimizes the total interest you pay over time, helping you keep more of your money.

Snowball Method (Best for Motivation)

Start by paying off your smallest debt first, regardless of interest rate. Once it’s paid off, roll that payment into the next debt. This creates quick wins that build momentum and keep you motivated.

Pay More Than the Minimum

Making only minimum payments keeps you in debt longer and costs you significantly more money in interest. Even adding a small extra amount—like $20, $50, or more each month—can dramatically speed up your progress.

Benefits of paying extra:

Reduces the total interest paid

Shortens your debt payoff timeline

Frees up more money for savings and investing

Whenever possible, use extra income—such as tax refunds, bonuses, or side hustle earnings—to make lump-sum payments. These one-time boosts can make a big impact on your overall debt balance.

Consider Consolidation or Balance Transfers

If you’re managing multiple high-interest accounts, simplifying your payments can help you regain control of your money. Two common options include:

Debt Consolidation Loans: Combine multiple debts into one loan with a lower interest rate

0% APR Balance Transfers: Move credit card balances to a card offering an introductory interest-free period

These strategies can:

Lower your overall interest rate

Simplify monthly payments

Help you pay off debt faster

⚠️ However, it’s important to read the fine print. Watch for fees, promotional periods, and interest rate changes to ensure the strategy truly benefits your money situation.

Step 4: Contribute to Retirement Accounts

Why Start Now

When it comes to building long-term wealth, time is your most valuable money advantage. The earlier you begin contributing to retirement accounts, the more you benefit from the power of compounding—where your money earns returns, and those returns generate even more money over time.

Even modest, consistent contributions can grow into substantial savings. For example, investing a small amount of money each month in your 20s or 30s can result in significantly more wealth than starting later with larger amounts. This is because your money has more time to grow and recover from market fluctuations.

Starting early also reduces pressure later in life. Instead of scrambling to catch up, you create a steady, sustainable plan where your money works for you in the background. Retirement becomes less overwhelming and far more achievable when you build the habit of investing regularly.

Employer Match = Free Money

One of the most powerful—and often overlooked—benefits of workplace retirement plans is the employer match. If your company offers a 401(k) with matching contributions, this is essentially free money added to your retirement savings.

For example, if your employer matches 50% of your contributions up to 6% of your salary, you should aim to contribute at least that 6%. Not doing so means you’re leaving valuable money on the table—money that could significantly boost your long-term financial growth.

Here’s why this matters:

It provides an instant return on your investment

It accelerates your retirement savings without extra effort

It strengthens your overall money strategy with minimal risk

Think of employer matching as a guaranteed boost to your portfolio—something that’s rare in the world of investing.

Build a Consistent Money Habit

To maximize results, automate your contributions so a portion of your paycheck goes directly into your retirement account. This removes the temptation to spend and ensures consistency.

Over time, increasing your contribution rate—even by 1% annually—can make a big difference. As your income grows, your retirement contributions should grow too, allowing your money to compound even faster.

The Bottom Line

Contributing to retirement accounts is not just about saving money—it’s about building future freedom. By starting early, taking advantage of employer matches, and staying consistent, you create a powerful financial foundation that supports your long-term goals and lifestyle.

Individual Retirement Accounts (IRAs)

| IRA Type | Tax Treatment | Key Benefit |

|---|---|---|

| Traditional IRA | Contributions may be tax-deductible | Reduces taxable income now |

| Roth IRA | Contributions made after-tax | Withdrawals in retirement are tax-free |

💡 Tip: No 401(k)? Open an IRA and automate your contributions. Even $25 per paycheck adds up!

Investment Options for Beginners

Use low-cost index funds or target-date funds for simple, diversified investing. These funds adjust automatically based on your retirement timeline and offer a balanced approach for long-term growth.

Step 5: Allocate Funds for Short and Long-Term Goals

Define Your Goals

Think about what you want to accomplish in the next year, five years, and beyond:

Short-term: vacation, new computer, holiday gifts

Medium-term: car purchase, wedding, moving costs

Long-term: home ownership, education, financial independence

Create Dedicated Accounts

Open individual savings accounts for each goal. Many banks allow you to name these accounts—”Vacation Fund,” “New Car,” etc. This helps you stay organized and track your progress.

Automate Contributions

Just like your emergency fund and retirement contributions, set up automatic transfers for goal-based savings. Even small amounts can make a big difference over time.

Use Sinking Funds

A sinking fund is a savings strategy for expenses you know are coming. For example, if you want to spend $1,200 on a vacation next year, save $100 per month. This prevents overspending or relying on credit.

Additional Tips for Post-Payday Success

Review Your Progress Monthly

Creating a monthly money check-in routine is essential for maintaining control over your finances and ensuring long-term success. Instead of guessing where your money goes, this habit gives you a clear, data-driven view of your financial life.

Start by reviewing your income, fixed expenses, and variable spending. Compare what you planned versus what actually happened. This helps you identify patterns—such as overspending on dining, subscriptions, or impulse purchases—that may be slowing down your progress.

Next, evaluate your financial goals. Are you consistently saving? Are you reducing debt as planned? Even small improvements in how you manage your money can lead to significant results over time. Adjust your strategy if needed—budgets are not meant to be rigid; they should evolve with your lifestyle.

To stay organized, use tools like budgeting apps, spreadsheets, or even a simple notebook. The key is consistency. A monthly review keeps your money strategy aligned, boosts motivation, and helps you stay focused on what truly matters—building financial stability and freedom.

Avoid Impulse Spending

Payday can create a false sense of financial freedom, making it easier to fall into the trap of impulse spending. While treating yourself occasionally is important, uncontrolled spending can quickly derail your money goals.

A highly effective technique is the 24-hour rule. Before making any non-essential purchase, wait at least a full day. This pause allows you to separate emotion from logic and evaluate whether the purchase truly adds value to your life.

During this time, ask yourself:

Is this purchase aligned with my money priorities?

Will I still want this tomorrow?

Is there a more affordable option?

By slowing down your decision-making process, you gain control over your spending habits. Over time, this simple practice can significantly improve your money discipline, helping you save more and spend with intention.

Take Advantage of Financial Education Resources

Investing in your money knowledge is one of the smartest decisions you can make. Financial education empowers you to make better choices, avoid common mistakes, and maximize your earning and saving potential.

There are countless accessible resources available today:

Blogs that offer practical tips on budgeting, saving, and investing

Podcasts that explain money concepts in a simple, engaging way

YouTube channels with tutorials and real-life financial strategies

Online courses that provide structured learning for long-term growth

Make it a habit to learn something new about money regularly—even just a few minutes a day can make a difference. The more you understand how money works, the more confident and strategic you become in managing it.

Over time, this continuous learning approach helps you build a stronger financial foundation, optimize your money decisions, and move closer to achieving your long-term financial goals.

Conclusion: From Surviving to Thriving

Breaking the paycheck-to-paycheck cycle is a powerful move toward financial freedom. When you take intentional steps right after payday—budgeting, saving, reducing debt, and investing—you reduce stress, gain control, and begin building a secure future.

Consistency is key. Even if you start small, your efforts will grow over time. With each paycheck, you’re not just covering bills—you’re investing in your peace of mind and financial independence.

Start today. Choose one step and act on it. Small wins lead to big victories—and a more confident, empowered financial life.